Top 10 LED Industry Trends in the year 2015

05-01-2015For many LED manufacturers, 2014 has been a prosperous and challenging year. Lighting market demands were stronger than expected in 1H14, leading to a period of LED supply shortages. Despite the positive development, the industry was impacted by clients double booking and distributors rising inventory levels during second half of the year. Many manufacturers were impacted by the markets cooling demands, and price competition as a result. As a result a lot of manufacturers’ performance in first and second half of the year was very polarized.

Facing the approaching year, below are some of LEDinside’s outlook for top 10 industry trends to watch out in 2015.

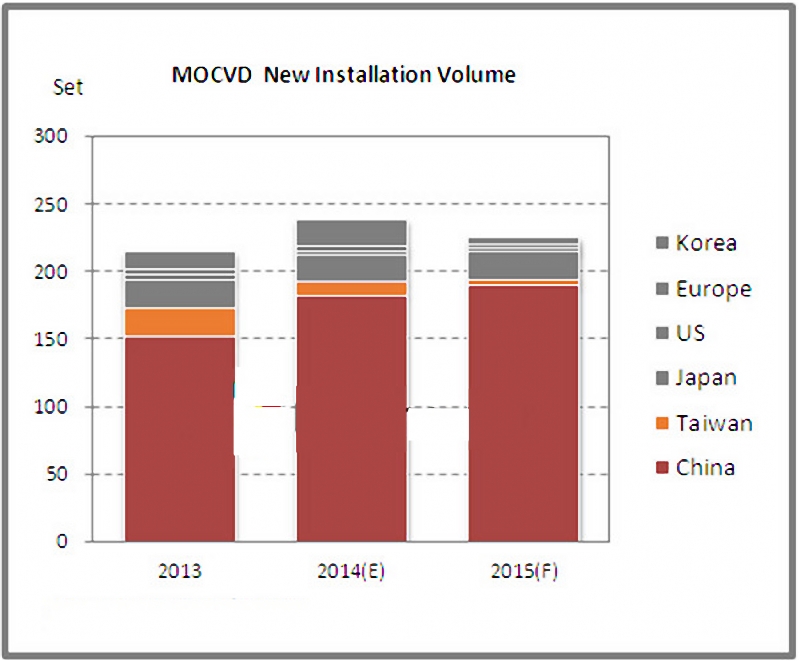

1. LED manufacturers expansion plans depend on government subsidies, China’s MOCVD installation volume remains largest

LEDinside estimates globally 239 new MOCVDs were installed. Based on regional MOCVD installation volumes, China remains the region with the most MOCVDs. Some local governments will continue to issue subsidies in China throughout the year 2015, therefore in certain areas in China more than 170 MOCVDs were newly installed. The Chinese government lowered subsidies, due to lower MOCVD costs. Currently, a single MOCVD subsidy was lowered from RMB 10 million (US $1.62 million) to RMB 5 million, and presents profitable opportunities for manufacturers. Overall, LED manufacturers expansion projects depends on local governments subsidies, hence LED chip manufacturers will grow in size.

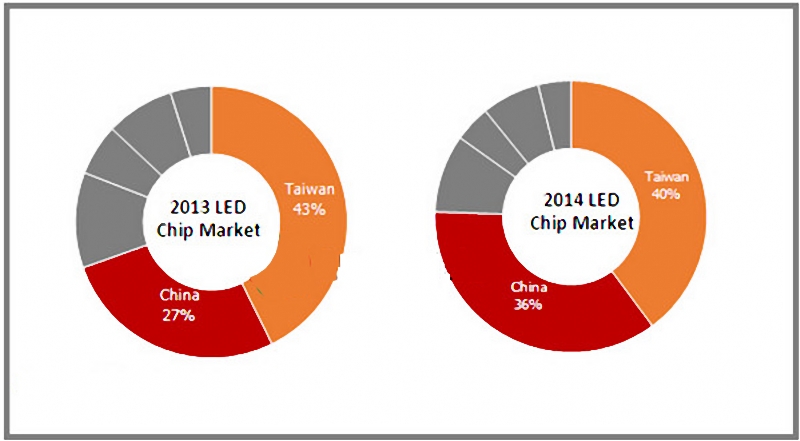

2. Chinese LED manufacturers market shares grow, big manufacturers become even larger

As Chinese LED chip manufacturers improve their technology and scale up production capacity, China’s LED chip production capacity increased from 27% in 2013 to 36% in 2014. In the past, Chinese LED backlight or lighting applications largely relied on Taiwanese or international LED manufacturers, but this is no longer the case. Due to Chinese package manufacturers increasing usage of domestic LED chips, prices are increasingly competitive, leading to Chinese manufacturers growing market share in the global LED industry.

3. LED lighting clients continue to seek low cost solutions

Spurred by falling product prices, high LED lighting market demands have emerged. LED bulbs remain the main growth drivers for LED lighting products in 2015, including LED bulbs, tubes and other light source products. Therefore, LEDs retail price and costs are often the main factors taken into consideration. Standard and mid-power LEDs with good C/P ratio often meet these LED lighting products lower price demands, for instance 3030 and 2835 LEDs have become mainstream on the market. Future LED manufacturers will continue to find better heat dissipation material, and use high driving currents to reduce the number of LEDs. Even COB LED has gradually attracted attention from lighting manufacturers. Besides LEDs lower prices, LED lighting manufacturers have also turned their focus to drivers and other components, in hopes of designing total solutions to lower costs.

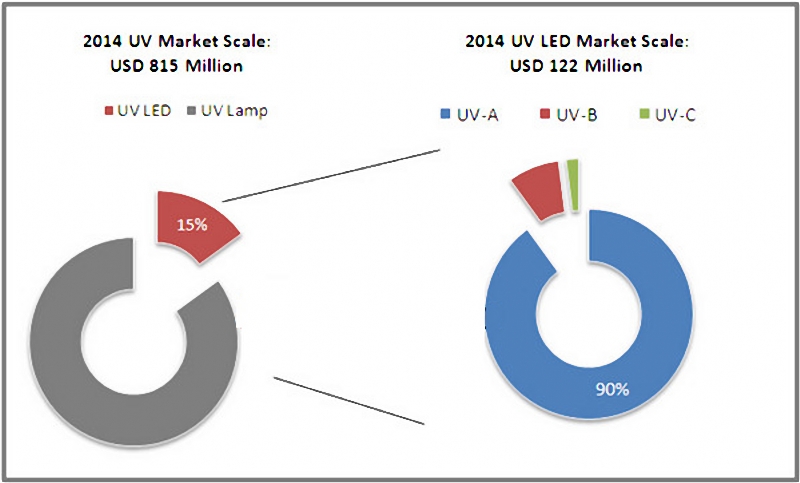

4. Finding special niche applications to raise profitability

Due to intense LED price competitions, LED manufacturers hope to find new applications to raise profitability. For instance, invisible LED lights including UV or IR LEDs are gradually becoming valued by LED manufacturers. Invisible LED light market remains a niche market, and cannot compare with LED lighting or backlight application volumes. The market sector has a much higher entry level, due to technology difficulties, customized demands, and close cooperation with system manufacturers. Therefore, invisible LED products gross profit margin is evidently better than white LED.

5. Growing automotive LED market value, exterior automotive lighting market showing highest growth

Automotive LED market grew steadily, with automotive Daylight Running Lamps (DRL) and high/low beam lights showing most significant growth. This is mainly due to high power LEDs technology advancement. Accompanying LED price falls, automotive LED has gradually shifted from high class car models to middle class models, which has spurred automotive lighting demands in the next few years. Additionally, car panel remain the largest LED backlight application in cars. Accompanying the spread of multimedia and image sensors, traditional clusters have all been changed to LCD panels to spur backlight demands.

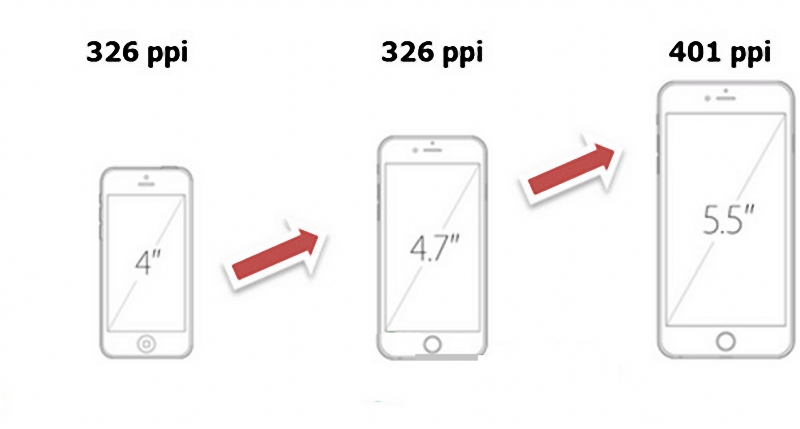

6. Mobile phones become thinner, smartphone backlight LED specs turn towards 0.4t

Currently, high-end smartphones are becoming thinner, with increasingly higher panel resolutions. This challenges LED manufacturers to make thinner and brighter LEDs in 2015. High-end smartphones use 0.4t LED as major backlight specs with brightness between 2,500-2,700 mcd. In 4.7”smartphones, 10-12 LEDs are used in the backlight modules, since 0.4t and 0.6t LEDs have become thinner, and are the slimmest LEDs in the mass produced backlight market. Package technology on the other hand has a much higher technology entry level. Japanese LED manufacturers have been the main suppliers for this technology. The 0.4t LED has been introduced into iPhone 6 backlight, and will even shift towards the thinner 0.3t LED in the future.

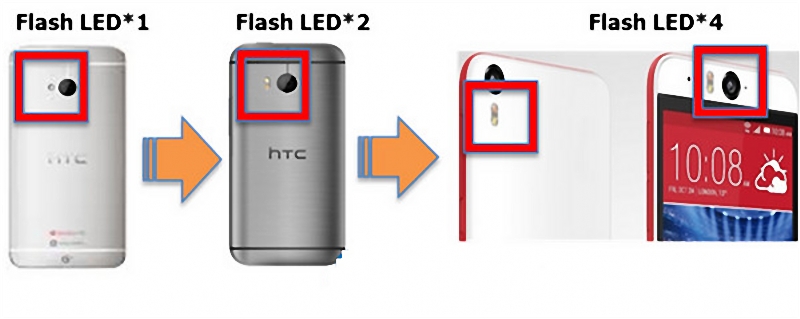

7. Flash LED usage volume gradually increases in high-end smartphones

Since iPhone introduced dual color temperature flash LEDs, more smartphone brands have also started to follow in their footsteps. Some smartphones have even added features and introduced 13 megapixel photo modules, equipped with four flash LEDs for the best photography effects. Flash LEDs brightness is between 180~240 lm range, with each smartphone using 1-2 LED pcs. As smartphone pixels increased, smartphone manufacturers flash LED demands also climbed up. Flash LED usage volume has continued to grow.

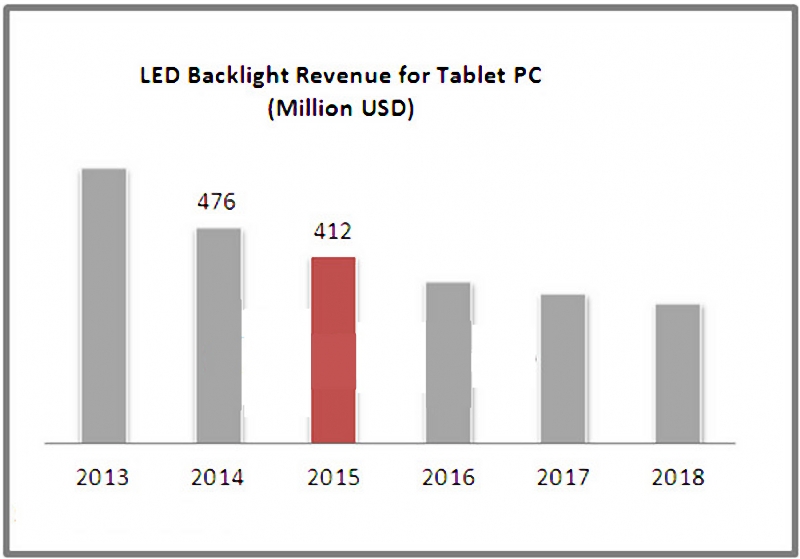

8. Declining tablet shipment volume affects backlight LED market value

In the past, tablet shipment volumes maintained a high growth trend, hence LED backlight usage in tablets was recognized by most manufacturers as possessing the highest growth potential. But in 2014, tablet shipments declined for the first time due to rising penetration rate and diminishing novelty. Tablets shipment volumes continued to decline in the future. However, sliding LED price, and tablet shipment volumes gradual decline led to LED market value to drop 21.7% YoY to US $476 million in 2014. By 2015, tablets LED backlight market value will plummet another 13.4% YoY to US $412 million.

9. LEDs for TV backlight applications shift towards reducing usage volume and raising color saturation

Accompanying improved LED backlight technology, price pressures from panel makers, which have led to TV backlight LED market gradually declined. In 2014, backlight LED market value will decline 14.3% YoY to US $2.39 billion, this downward trend is expected to continue into 2015, estimated LEDinside.

Observations on LED backlight specs pointed the industry will be moving towards two different development directions in the future. In standard and mid end TVs, LED is requested to use higher driving current to reduce total LED usage volume, further in order to lower costs. However, in high-end TV models, raising LED brightness to satisfy 4K2K panel demands, and the introduction of NTSC 100 highly color gamut will also become a development focus for LED manufacturers.

10. Small pitch display increasing market penetration becomes major growth momentum in display market

LED display field is becoming increasingly mature and saturated, despite the positive impact from Brazil World Cup in 2014, which stimulated the global LED display market demand. However, the future outlook is with fewer large sports events to spur public expenditure, the market will need to depend on the introduction of new technologies in the near future, such as small pitch display and other products to create new market demands.

©Copyright: 2008-2026 Guangzhou TEEHON Electronics Co., LTD.